Offices around the world are transforming. Take Singapore’s 18 Cross. Originally constructed in the early 2000s, the building has been upgraded to meet Grade A office standards in a mixed-use retrofit project that maximises natural light and includes a 20-metre ‘green wall’.

Sustainability was at the heart of the scheme, which incorporates features such as solar energy, rainwater harvesting, and electric-vehicle charging and bike parking facilities.

It’s a project that reflects two key trends preoccupying the owners of older commercial buildings. First, the decarbonisation goals of national governments have pushed regulators and cities worldwide to ratchet up sustainability requirements for offices. Second, occupiers, faced with their own net zero commitments, increasingly require offices with high environmental performance and are often willing to pay a premium to get them.

As a result, landlords with underperforming buildings face an imperative to decarbonise, both to ensure regulatory compliance and to maintain their assets’ appeal to tenants. The question is how: should they optimise their existing offices, carry out a retrofit or opt for a sustainable redevlopment?

A tightening decarbonisation regulatory framework

The scale of the issue is significant. According to the World Economic Forum, an estimated 80% of buildings in cities that will be in use in 2050 in most mature markets have already been built, many before the introduction of modern energy efficiency standards. As Joanna Conceicao, Director, Savills Earth, says: “Building owners are faced with an enormous upgrade challenge to get this stock in line with regulatory requirements and market expectations that are already in place and getting stricter with time.”

In many major markets, the majority of overall office stock requires investment to meet tightening upcoming or proposed environmental performance standards by 2030. For example, the Tertiary Decree in Paris requires a substantial proportion of office buildings to reduce energy consumption by 40% by 2030. Elsewhere in London, proposed Minimum Energy Efficiency Standards require at least an Energy Performance Certificate ‘B’ rating by 2030, with 61% of office buildings currently below this standard.

Offices requiring investment to meet higher environmental standards

Source: Savills Research. Note: Reflects percentage of total office buildings requiring intervention to meet tightening regulatory standards by 2030.

In the European Union, the Energy Performance of Buildings Directive (EPBD) will require the renovation of over a quarter of the worst-performing commercial buildings by 2033. In New York, the Local Law 97 caps annual emissions from buildings and imposes fines where this is exceeded, with 64% of buildings currently expected to be non-compliant in 2030.

Elsewhere, Sydney is witnessing a step change towards electrification of its office stock. New large commercial buildings will be required to be all-electric by 2027, but we are also seeing a trend for existing Grade A stock to include the electrification of heating as part of wider retrofit interventions.

The options: optimisation, retrofit or redevelopment

What are the strategic options available to commercial building owners with underperforming assets? In essence, there are four decarbonisation pathways:

- Building optimisation involves simple, low-cost improvements such as upgrading building management systems or installing lighting sensors. They cause minimal disruption to tenants but rarely bring a significant uplift to a building’s performance.

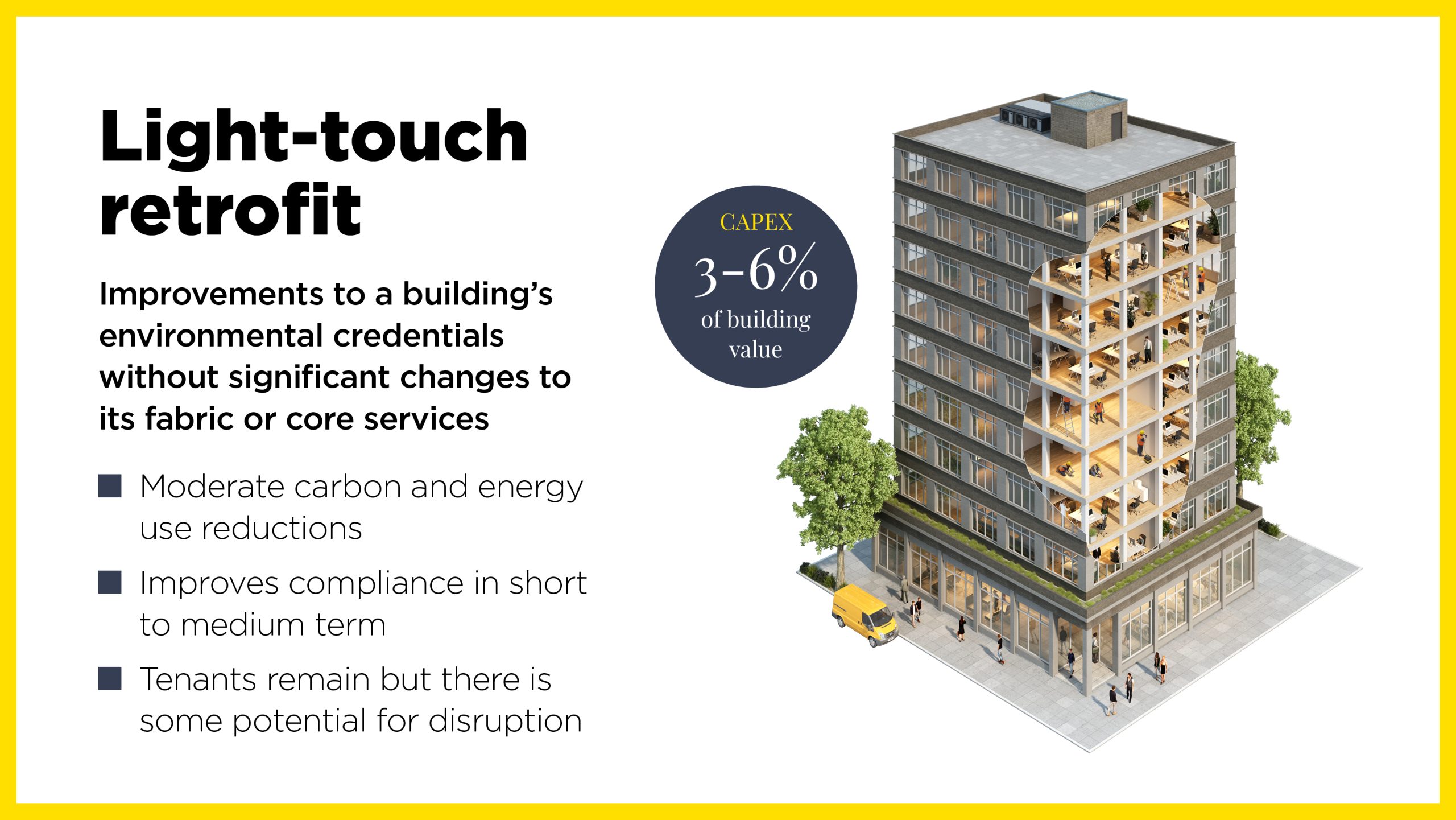

- Light-touch retrofits deliver moderate energy performance upgrades without significant changes to the building fabric or core services. Offices remain occupied, but there is some disruption to tenants.

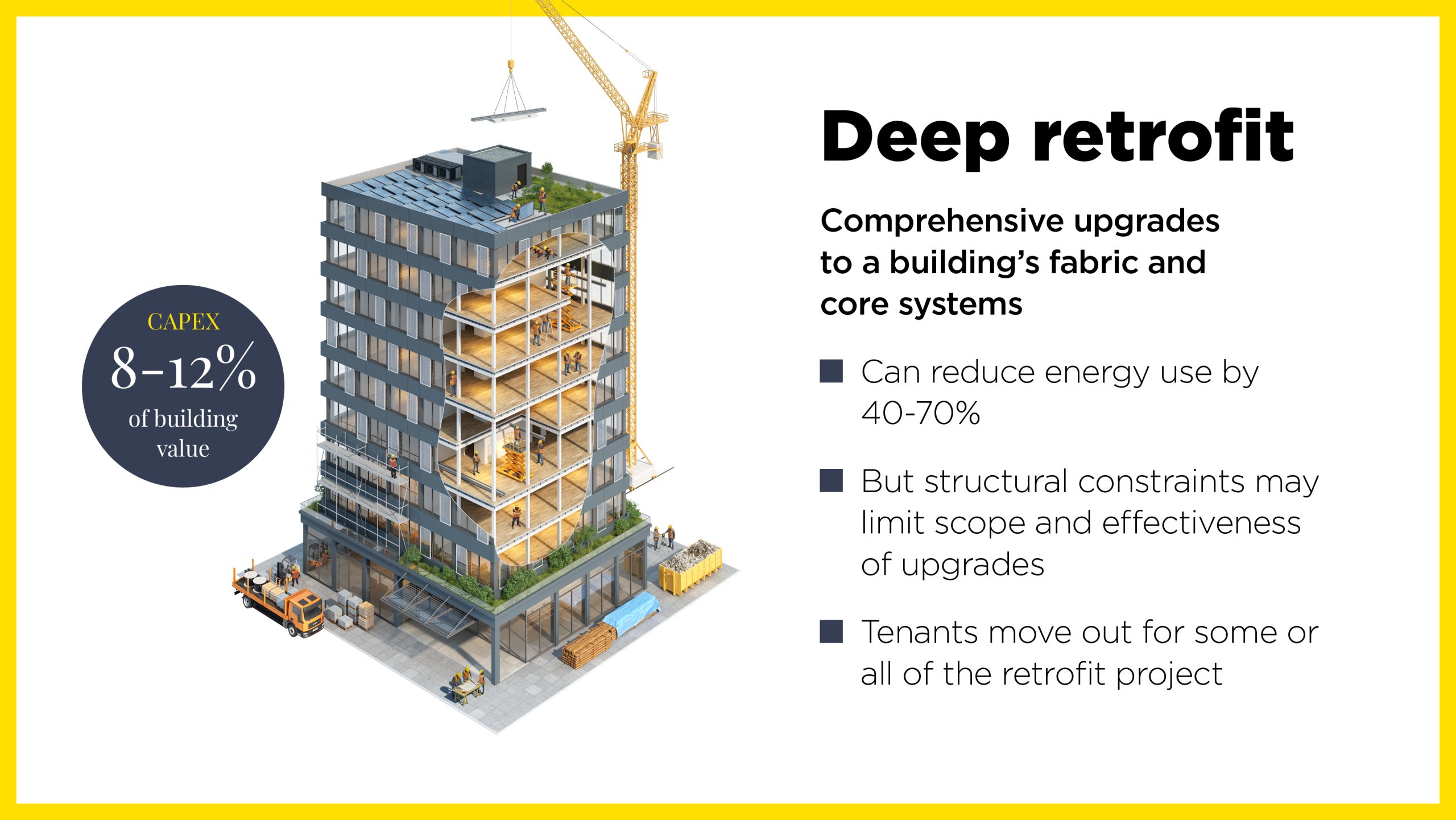

- Deep retrofits are major upgrades to a building’s fabric and core systems, which can include reconfiguring layouts, electrifying heating systems and upgrading ventilation and cooling infrastructure. They are capital-intensive and require tenants to move out for some or all of the time, but can cut carbon impact by 40-70%.

- Redevelopment involves demolishing existing offices and replacing them. It can bring the greatest reduction in operational carbon (the emissions generated by the energy used to run the building), but has the highest cost, delivery risk and embodied carbon (the emissions generated by a building’s materials and construction).

Owners must weigh up a range of factors when determining the best pathway, including the sustainability benefits, local regulatory and market environment, costs and financial returns, and the ease of adapting the existing building.

Assessing the carbon impact

Determining the potential carbon impact of retrofitting or redeveloping offices is complex, as it requires considering both embodied and operational carbon across their full life cycle (known as whole-life emissions) – from the manufacture of materials and construction, through occupation, to demolition and beyond.

Offices have become operationally more efficient in recent years, a trend that will accelerate as the grid decarbonises. As a result, embodied carbon is becoming responsible for a larger proportion of buildings’ emissions. By 2050, it will account for 49% of whole-life emissions in new construction, compared with 25% in 2021.

Projected carbon emissions from global new construction to 2050

Source: Savills Research using UN Environment Programme

It’s a trend that favours retrofitting offices, but structural or viability constraints mean this is not always the best option. Thoughtfully designed new buildings can deliver lower operational carbon than retrofitted assets, as well as benefits for tenants and the community. Advances in lower-carbon alternative materials in new developments can also mitigate the carbon impact.

The growth of circular approaches in construction can also reduce the embodied carbon footprint of a new development. A joint study by the World Economic Forum and McKinsey found that a circular approach prioritising the reuse of materials could reduce the carbon impact of new builds by almost 75% in 2050. “At the moment, retrofit is almost always better than redevelopment on a sustainability analysis because it has lower embodied carbon,” says Nuno Fideles, Head of Sustainability, Savills Portugal.

“But as the circular economy becomes more mature, an increasing proportion of a new building’s materials will be reused – helping to narrow the embodied carbon gap.”

The ability to do this is, however, reliant on local ecosystems of companies to take and trade reclaimed materials, and local regulations or policies encouraging the circular economy. The Savills Material Reuse Materiality Index analyses how this varies in different cities around the world, with London and Amsterdam leading the way.

Savills Material Reuse Maturity Index

Source: Savills Research

What’s possible with a retrofit?

There can be technical limits to what retrofit projects can deliver. Office occupiers are increasingly prioritising well-being, with good natural light, consistent temperatures and high air quality seen as essentials. Often, the structures of older buildings, with lower floor-ceiling heights and inflexible layouts, can’t be adapted to this. In some cases, the thermal or overall carbon performance can’t be sufficiently upgraded either.

In contrast, new offices can be developed using a ‘long-life, loose-fit’ approach that can adapt to changing user needs over a building’s lifetime. A well-designed, adaptable new building is also likely to offer greater resilience against a changing climate.

The financial case for office upgrade investments

When considering investment in existing stock, building owners balance factors including capital expenditure, risk of vacancies, planning risk, exit yields and the potential increase in rents. The owner’s access to capital and risk appetite will also play into that assessment.

Some landlords may opt for building optimisation or a light-touch retrofit to meet immediate compliance and occupier requirements before considering more capital-intensive options at a later stage.

Building optimisation is typically less than 2% of a building’s value, with light-touch retrofit around 3-6%. The risks are relatively low: tenants typically don’t move out, so no rent is lost, and there is no (or limited) planning risk. However, there is little prospect of significantly increasing rents.

The costs and risks of other interventions are higher, but the rewards can be greater, too. Both deep retrofit and redevelopment entail vacant periods and extensive planning and construction risk.

Deep retrofit typically costs 8-12% of a building’s value. But the scarcity of premium office space in some markets means that high-quality retrofits can command significant rent increases. For example, successful projects outperformed average rental growth by 57% in Madrid and 67% in New York over an average four-year time frame.

“The decision between retrofit and redevelopment is rarely binary,” says Michael Glatt, President, North America Project Management, Savills.

“Redevelopment can unlock transformational value and deliver highly efficient, future-ready space – but it carries greater capital exposure, planning complexity and delivery risk. Retrofitting, on the other hand, can preserve embodied carbon and maximise the use of existing assets, though it often requires careful navigation of legacy infrastructure and structural constraints.”

It’s time to deliver on decarbonisation

Deciding on the best way to decarbonise an office building involves navigating a complex set of trade-offs. While retrofitting should be the priority for existing buildings, it will not always be the right solution.

These options are also not mutually exclusive. For many assets, the most effective strategy is a phased approach – combining near-term optimisation measures with more substantial retrofit interventions over time, aligned with lease events, capital cycles and asset repositioning. This might mean optimising performance today, delivering a light-touch retrofit in the medium term and planning for a deeper retrofit or rebuild when opportunities arise.

Glatt adds: “The most successful strategies don’t default to one approach over the other – they rigorously evaluate both financial and non-financial factors, including sustainability, operational performance, risk profile and long-term flexibility. Increasingly, we’re seeing clients look for hybrid solutions that retain and reuse valuable components while selectively redeveloping where it drives real performance gains.”

Where redevelopment is pursued, the focus must be on minimising whole-life carbon and delivering long-term impact – environmentally, socially and economically. This includes embedding circular principles from demolition to construction, prioritising low-carbon material choices and designing buildings with flexibility, adaptability and climate resilience in mind. Done well, redevelopment can strengthen connections with local communities, particularly through active and engaging ground-floor uses.

The right approach will vary by asset, but those who align decarbonisation strategies with a building’s potential and market demand will be best placed to deliver lasting value.

Lisbon: the transformation of MB4

The MB4 building in central Lisbon has undergone a deep retrofit that has transformed the 14,000 sq m space. The 40-year-old building now offers flexible accommodation for tenants, wellness spaces, a café, an auditorium, a bike park and a transformed ground floor that has been designed to be an engaging public space. Structural changes have enabled access for people with reduced mobility, and the building has achieved BREEAM In-Use ‘Excellent’ certification.

Beijing: from electronic market to high-quality offices

Growing demand for offices in Beijing’s ‘Silicon Valley’ led to the decision to convert the 200,000 sq m Ding Hao 3 electronic market building into high-quality office space. The retrofit project – which reflects the Beijing city government’s focus on reusing existing buildings rather than a ‘build and scrap’ approach – achieved Gold LEED certification and has cut carbon emissions by an estimated 60% compared with demolition and redevelopment.

David Forbes

Co-founder, Enright Capital

Enright Capital invests in, develops and manages commercial property in Calgary, Canada. We acquire Grade A and B office buildings and generate returns by retrofitting and refurbishing them.

In a market with average occupancy of 70-80%, we typically purchase buildings that are 50-65% leased. They generate income of around 8-10% of their acquisition prices at the time of purchase, supporting conventional financing. These buildings have often become less attractive to occupiers because the previous owners have been reluctant to reinvest capital in them.

Our approach centres on repositioning assets to align with modern occupier expectations. This includes building multiple move-in-ready show suites, upgrading common areas and adding amenities such as fitness centres, conference facilities and tenant lounges.

We focus on leasing to small and medium-sized enterprises. While this increases leasing and management costs, it enables stronger lease terms due to reduced competition from landlords in this segment. A diversified tenant base also enhances income resilience.

Our target is to achieve stabilised occupancy of 90%. Currently, average occupancy across our portfolio is 98%. As income grows, we focus on refinancing our assets to fund further improvements and return capital to investors.