The past five years have been characterised by a structural return of inflation, a rebasing in interest rates and an increase in volatility.

At the same time, we have seen rapid technological progress, a rise in populist governments and increased global fragmentation. The current environment contrasts sharply with the era of ‘Great Moderation’, a period of relative macroeconomic stability spanning the previous several decades.

There has been a structural shift in the established rules governing the behaviour of economies and financial markets, disrupting investors’ preconceptions around how different parts of the system interact. In this new regime – let’s call it the era of ‘Great Volatility’ – the investment landscape has changed.

We have seen the emergence and adoption of new asset classes, such as digital assets, whose tangible value is still being debated. Meanwhile, old asset classes have started behaving differently, leaving question marks over relationships investors previously took for granted.

Bond market volatility has increased. This is mostly due to the return of inflation, but it’s also because, in this new era, bonds are not as ‘risk-free’ as they once were. Gold has gone from being the ultimate safe-haven asset to one driven by speculative capital. The US dollar has depreciated during periods of global risk-off behaviour, prompting speculation about its continued position as the global reserve currency.

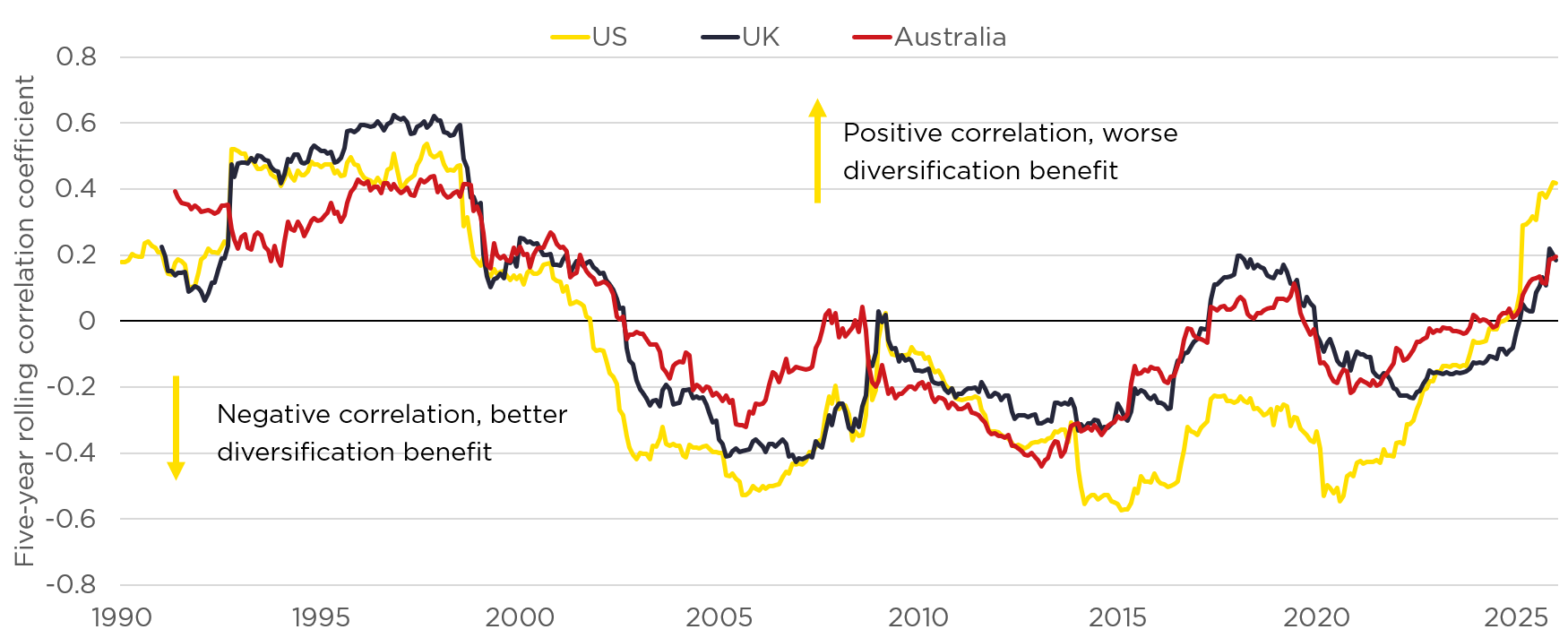

From an asset management perspective, perhaps the most significant ramification of this structural shift is the breakdown in the relationship between equities and bonds – or, at least, a return to the pre-2000s relationship of positive correlation. If fixed income can no longer provide an effective hedge for higher-risk equities, it brings into question the modern-day relevance of the 60:40 portfolio, which has been a mainstay of investment strategy and portfolio construction over recent decades.

Equity bond correlation

Source: Savills Research using Macrobond. Based on total return, benchmark equity indices and 10-year government bond. Correlation coefficient is a statistical measure ranging from -1 to +1 that quantifies the strength and direction of a the relationship between two variables.

Is real estate a safe-haven asset?

With the US dollar, gold and equity-bond correlations all behaving atypically, the question becomes: where should investors seek safety in the current investment landscape?

Real estate is often regarded as a safe-haven asset, but the reality is more complex. Safety can mean different things for different investors, but there are some common characteristics. Safe-haven assets typically need to be highly liquid, able to retain or increase their value through periods of economic stress, and be uncorrelated with a reference market. They have minimal or zero credit risk and their value is often anchored by a tangible purpose, or scarcity of supply.

Which assets can provide these characteristics? Gold and other precious metals, which retain both commercial and retail value, satisfy the conditions of liquidity, tangibility and scarcity. Currencies such as the US dollar, Japanese yen and Swiss franc, which are issued by stable democracies in countries with strong institutions and open capital markets, also respond to safe-haven demand. Government bonds can increase in value during periods of economic uncertainty. They are generally liquid and have a low default risk, often being referred to as the ‘risk-free’ benchmark (although only in countries with low political risk and credible fiscal records).

Clearly, property does not satisfy all these conditions. It is not liquid, and it can carry credit risk, depending on the underlying tenant base or debt provider. Large transaction sizes can also concentrate exposure to a single economy, sector or tenant, introducing further risk. Investors need significant capital to build a diversified portfolio from both geographic and sectoral perspectives (although pooled investment vehicles can mitigate against this risk).

This concentration can accentuate exposure to black swan events if assets are located in proximity. In the aftermath of Russia’s invasion of Ukraine, for example, many global corporations incurred significant financial losses due to divestments, write-offs or outright seizures of their Russian operations, including real estate holdings. Generally speaking, the more physical and immobile the asset, the larger the write-off.

Finally, real estate is a GDP-linked asset class. Total returns are correlated with the performance of the wider economy – albeit with a lag – driven by trends in employment, consumer spending and trade. That makes them inherently cyclical.

All that said, property is tangible, with a clear functionality and purpose to support its returns. Land is a scarce resource that will retain some value through economic cycles, even in an extreme scenario where the bricks and mortar themselves become obsolete. Rental income, meanwhile, can provide steady returns during periods of uncertainty, even if capital values are more volatile.

In the UK, for example, the average annual income return from real estate during periods of recession was 5.7%, a mere 20 basis points below the non-recessionary average of 5.9%, according to MSCI data spanning the past 55 years.

Property retains its diversification benefits

A more important factor, however, is that real estate returns are uncorrelated with other asset classes, and particularly with equities. Indeed, diversification is routinely cited as the raison d’être for real estate investment. “What we’re seeing globally is a reset in how investors think about diversification,” says Neil Brooks, Head of Asia Pacific Capital Markets, Savills. “With equities and bonds increasingly moving together, real estate’s combination of income, tangible value and portfolio diversification is once again becoming central to institutional asset allocation.”

Real estate’s diversification potential is underpinned by its heterogeneous nature, the long-term-orientated investor base and relatively stable underlying cashflow. It is also a function of infrequent valuations. Indeed, illiquidity is often cited as a reason for investing in private markets more broadly, not only because it can boost returns through the ‘illiquidity premium’, but also because it reduces volatility across a wider portfolio.

This dynamic was evident during the most recent cycle. Global developed market equities, as represented by the MSCI World IMI Index, declined by nearly 22% peak-to-trough between January and October 2022, driven by Covid-19-related supply-chain disruptions and Russia’s invasion of Ukraine. Over the same period, the MSCI Global Property Index returned a positive 5%. Real estate values only began to correct in late 2022, by which point equity markets had already passed the bottom.

With low volatility and a diversified return profile, the evidence shows that, over the long term, an allocation to real estate can boost overall returns, particularly on a risk-adjusted basis. This appears unchanged in the era of Great Volatility. Based on US data, private real estate continued to be negatively correlated with the major investible asset classes, including equities, government and corporate bonds, and gold, from 2021-25. Furthermore, on a risk-adjusted basis, private real estate continues to occupy the sweet spot between equities and fixed income.

US private real estate total return correlations

Source: Savills Research using Macrobond and S&P Global. Private real estate based on the NCREIF Property Index.

The benefits of diversification become even more important in a world where it is increasingly challenging to find. As outlined above, equity and bond correlation is now positive, negating the benefits of using fixed income to hedge stock prices.

Geographical and sectoral diversification is also diminished: world markets are more correlated now than in past decades, driven by a more globalised economy, increasingly synchronised monetary policy cycles and the greater availability and speed of information. Meanwhile, benchmark equity markets are more narrowly concentrated, particularly in the US, where concentration is at its highest level for at least 100 years, according to the UBS Global Investment Returns Yearbook.

A partial hedge against inflation

A defining feature of the era of Great Volatility is the return of inflation. Across the OECD group of developed economies, inflation has averaged nearly 6% over the five-year period from 2021-25, more than double the rate over the previous two decades. While real estate is widely held up as a good hedge for inflation, here too, the reality is more nuanced.

The characteristics required to protect against inflation are similar to those that support safe-haven demand. Tangibility means an asset’s value is more likely to follow underlying price trends, while scarcity provides pricing power for asset owners to pass on rising costs.

For real estate, tangibility and scarcity generally apply. Some property also has a direct link with inflation through the structure of lease agreements (for example, index-linked leases, turnover rents and triple net agreements). However, there are important sectoral and geographic distinctions, and the cyclicality of underlying returns implies that the underlying driver of inflation influences real estate’s effectiveness as a hedge.

Why real estate still belongs in investor portfolios

So where does real estate sit in today’s investment landscape? Essentially, it is where it has always been. With change everywhere, the ‘world’s oldest asset class’ remains largely true to itself. As Rasheed Hassan, Head of Global Cross Border Investment, Savills, says: “Real estate continues to provide a good diversification to other asset classes, including equities, while helping to reduce overall portfolio volatility.

“It also continues to deliver a relatively stable income through the economic cycle and sits in the sweet spot between fixed income and equities in the risk-return profile, providing both income and capital growth.” On top of this, real estate can provide investors with a viable safe haven during periods of market volatility, as well as some protection against inflation.

This consistency is reflected in the preferences of major global capital allocators. Despite all the flux that now defines the era of Great Volatility, institutional allocations to real estate have held steady at nearly 11% since the beginning of the decade. Now is certainly not the time to reduce those allocations because, as a point of entry, global real estate is starting to look attractive relative to other asset classes.

Global institutional target allocations to real estate

Source: Savills Research using Cornell University/Hodes Weill & Associates Real Estate Institutional Allocations Monitor

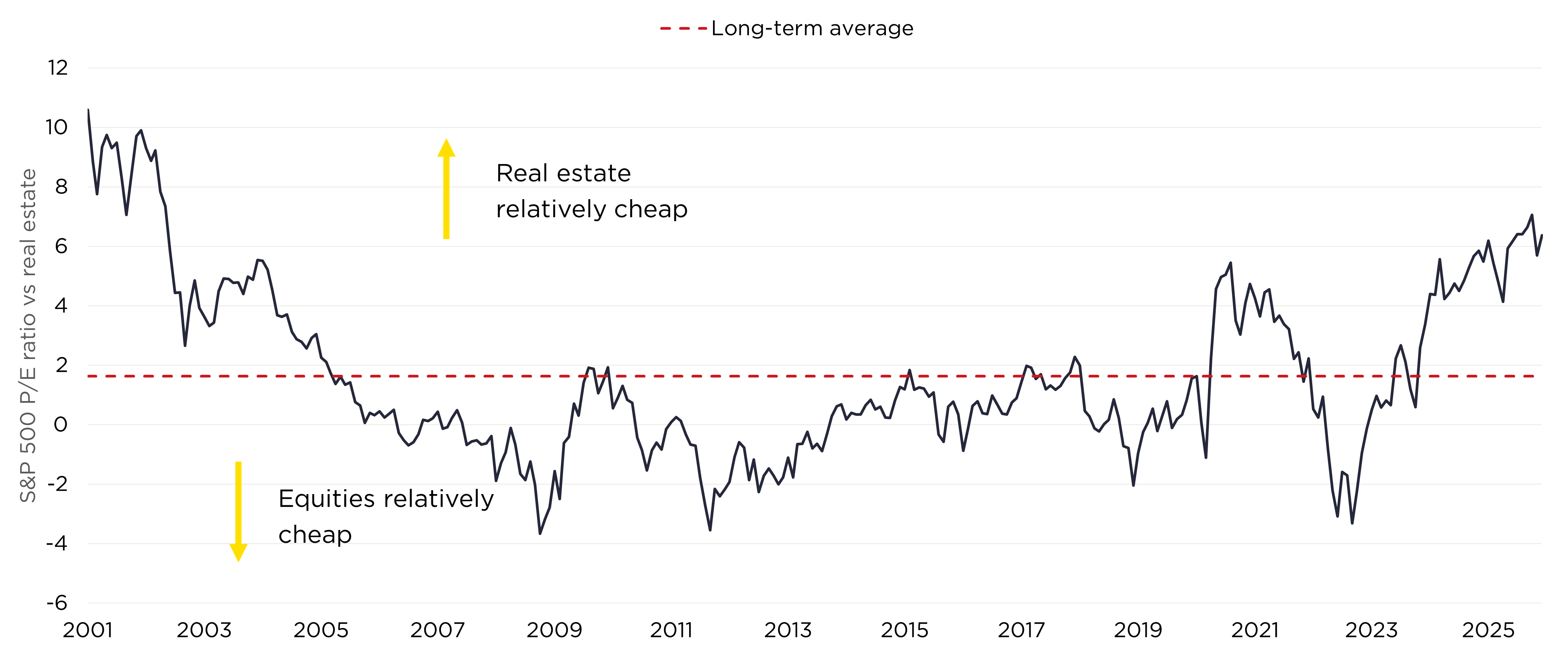

This is particularly true relative to equities. Global stock prices have nearly doubled over the past three years. Such an increase is rare. Over the course of 150 years in the US, for example, it has only occurred three times: in the lead up to, and subsequent recovery from, the Great Depression in the 1930s; during a stock market boom in the mid-1950s; and through the dot-com bubble of the late 1990s.

This has driven valuations to near record highs, as measured by the price-to-earnings ratio. Based on historical data, investing in the S&P 500 at the current valuation would deliver annual returns of around 2% over a five-year investment horizon, barely keeping up with expected inflation. Other geographies show a similar dynamic. In the UK, for example, the expected annualised five-year forward return would be less than 5%.

Real estate, therefore, enters the new era not as a sector looking for relevance, but as an asset class whose long-established virtues remain valid – and one of the few asset classes where today’s entry point looks compelling.

Relative valuation of US direct real estate vs S&P 500

Source:Savills Research using Macrobond and MSCI RCA. Direct real estate P/E ratio calculated as the inverse of a blended cap rate.

Martin Towns

Global Head of Real Estate, M&G Investments

“Real estate has tested the patience of investors in recent years, but it is now firmly back on the agenda for asset allocators.

Following a period of underperformance relative to public markets – and, in some cases, significant value destruction that has been driven by structural change – the asset class has reset.

As capital returns to the sector, we are seeing the fundamental strengths of real estate reassert themselves. Income, diversification and inflation linkage are once again differentiating property – and this is happening at a time when equities and bonds are increasingly moving in tandem, and geopolitical risk continues to inject volatility into the public markets.

Valuations have adjusted meaningfully, prompting an improvement in the relative appeal of real estate. However, the performance of assets will not be uniform. Returns will be driven by selectivity: investing in places that endure, and buildings that are capable of meeting the complex needs of a changing economy.

The opportunity is clear, but investors who want to make the most of it will need to take an active, disciplined approach. There is no room at all for complacency: this will not be a market that rewards passive capital.”